Starting with disclaimer that I am not related to any insurance company,consider my couple of real time experiences ..of course names used are arbitrary.

Rajesh was paying Rs.80,000 annual premium towards his endowment plans.When he find all his policies are not going to offer him great returns then he surrendered all in mid 2009.But he never save / invest any money which he was earlier paying towards premium of life insurance.

Mahesh surrendered all his insurance plans and started investing in mutual funds throuh systematic plans.But not able to stick to SIPs as mutual funds were not able to generate even after investing for three years.

So these are two experiences I have from my friend circles where they have surrendered their policies without any concrete investment plans.

Its quite true that insurance plans are not going to generate any great returns for you in future.When I analyse returns on LIC Money Back Policy I found them around 6-6.5%.I just want to continue in this plan as premium is a level premium which will remain constant & its like Forced saving account where I am sure that I will force my self to save under motivation of lapsation of policy.While in case of other instruments like PPF its always an arbitrary contribution.

So just coming back to issue of surrendering any insurance plan,I think few questions need to be asked :

- What is motive of surrendering – Is it because I am not going to get any great returns,I am not able to manage my finances or its creating conflicts for important events like buying home.

- Are you ready with concrete plan to invest money which you are going to save after exiting the insurance policies – it may be anything like mutual funds,real estate etc..

- Suppose if you started investing in equities what will be your reaction if there is sudden break down in the market?

- What will be your reaction if there is loss of 10% after investing systematically over a period 3 years?

- What do you think – fixed deposits or recurring deposits are alternatives especially if you are in highest tax bracket?

I think one should get answers of above questions and then think to surrender the plan….as its irreversible process to reinstate once you surrendered.

Bottomline:

Having number of insurance policies is not less than illness of the portfolio, but if you are thinking to exit without any concrete plan then its like “Cure is worst than the illness”..isn’t it?What do you think?

Related Posts

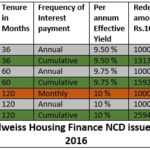

10% Edelweiss Housing Finance NCD Issue July 2016:

10% Edelweiss Housing Finance NCD Issue July 2016: DSP BlackRock Mutual Fund – Dynamic Asset Allocation fund – New concept – Pros & Cons

DSP BlackRock Mutual Fund – Dynamic Asset Allocation fund – New concept – Pros & Cons Check IFCI Tax Saving Series-3 Allotment:

Check IFCI Tax Saving Series-3 Allotment: IDBI CGAS-1988 Account,LIC’s New Jeevan Nidhi,LIC Flexi Plus,ICICI Prudential Online Child Plan

IDBI CGAS-1988 Account,LIC’s New Jeevan Nidhi,LIC Flexi Plus,ICICI Prudential Online Child Plan What Is EUIN – Employee Unique Identification Number

What Is EUIN – Employee Unique Identification Number Check Allotment status Of PFC Tax Free Bonds 2013:

Check Allotment status Of PFC Tax Free Bonds 2013:

Well written and concise..it makes one think why we should think before surrendering a policy !

thanks for the comment.

Policy surrendering is only half way & needs to be done considering all the factors.

By the way Currently I am facing some problems on comment side and few comments are not appearing.